The most important digital payment trends 2023 in Switzerland

The most important digital payment trends 2023 in Switzerland

Melanie

Frutiger

2022 was once again a turbulent year. The Covid pandemic lingered, the Russian-Ukrainian war broke out, the energy and raw materials crisis intensified, inflation soared, and consumer spending plummeted. The consequences of all this — and more — were felt in online trading: The boom from the lockdowns was over.

And yet, this year has also taught us a lot, perhaps even more than we think. The difficult times have made e-commerce more resilient: companies became more flexible to stay competitive. And the future of payments is definitely digital.

In this article, the Swiss online payment service provider Payrexx explains current and future trends that will shape and influence digital payments in 2023 in Switzerland. Online merchants should keep an eye on them.

Trend 1: Mobile Payment and Wallets become the new standard

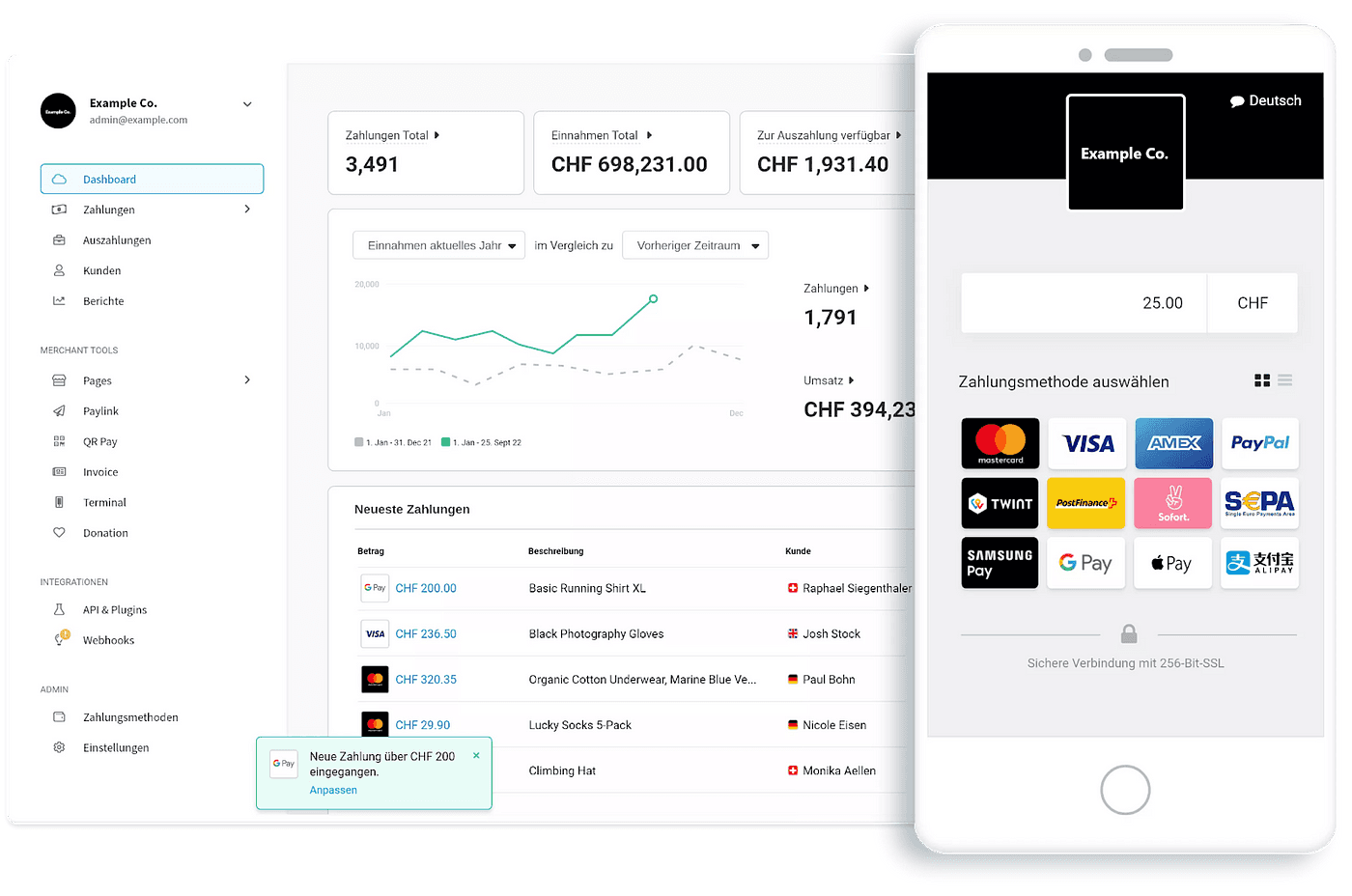

Paying by smartphone is becoming increasingly popular, and in 2023 most customers will make their payments using mobile payment applications like Apple Pay, Google Pay, Paypal (in Switzerland primarily e-commerce), TWINT, and Samsung Pay.

These applications offer a convenient and secure way to make payments and are becoming increasingly important, especially in the e-commerce sector. Using NFC technology (Near Field Communication, abbreviated as NFC, is a short-range wireless technology that allows devices to communicate when they are in close proximity of about ten centimeters) and QR codes, customers can make contactless payments easily and quickly using their smartphones or wearables. For companies, it will be essential to offer these payment options.

Trend 2: Growth of QR code-based payments

In recent years, QR code-based payments have become increasingly established, and in 2023 they will play an important role in digital payments.

First of all, it is important to understand how QR code-based payments work. QR codes are two-dimensional barcodes that can be scanned using a smartphone camera. Once the QR code is scanned, the user is automatically redirected to a payment page where they can complete the transaction. This simple and convenient payment method offers many advantages for both customers and companies. For customers, it means they don’t need a special payment card or hardware to make a payment. They can simply use their smartphone to scan the QR code and complete the payment. For companies, the growth of QR code-based payments means they can offer their customers a fast and convenient payment method without having to install special hardware or payment terminals. This can be particularly beneficial for smaller companies that cannot afford the cost of installing payment terminals.

An example of the growth of QR code-based payments is the Chinese online retailer Alibaba, which enables its customers with a simple and convenient payment system using QR codes. In Switzerland, QR codes are primarily known in connection with TWINT and the new Swiss QR bill. Payrexx has developed a simple QR code solution for SMEs that supports not only TWINT but all relevant payment methods in Switzerland.

Trend 3: Increase in “Buy now, pay later” (BNPL) payments, online, but also in-store

“Buy now, pay later” (BNPL) is a payment method that allows customers to make purchases immediately but defer payment to a later date.

BNPL has gained popularity in recent years and has become a global trend in digital payments. One of the main reasons for the increasing popularity of BNPL is that it is particularly attractive to younger consumers who may have limited financial resources and find it difficult to pay for larger purchases all at once. In addition, the payment process is very flexible and secure.

Finally, the COVID-19 pandemic has contributed to BNPL becoming a trend, as many people have become more cautious about spending money due to economic uncertainties and restrictions on physical shopping, looking for alternative payment options like BNPL that allow them to make purchases without having to provide the full amount of money all at once.

In fact, the trend could become a permanent and attractive solution for younger generations in Switzerland. The benefits for consumers include:

Payment is not required until after receipt and inspection of the goods, often making refunds to end customers unnecessary.

Larger purchases can be made without prior saving.

The processing via the payment service provider apps is intuitive and secure.

However, there are also drawbacks and risks that everyone should be aware of if they wish to make purchases with deferred payment in the future:

additional fees in the event of late payment

credit limit often non-transparent

payment deadlines not always adjustable

According to the Online Retailer Survey 2022 — a study by the E-Commerce Lab of the Zurich University of Applied Sciences (ZHAW), two-thirds of retailers offering BNPL see benefits mainly in attracting additional customers through a broader range of payment options, as well as in higher conversion rates, greater loyalty of existing customers, and constant availability of this payment method.

Ivan Schmid, CEO and founder of Payrexx, expects that BNPL will also catch on in-store and in the B2B sector, as more and more business processes are digitized and it allows companies (especially young start-ups) to improve their cash flow situation by deferring the payment of purchases to a later date.

In Switzerland, the following BNPL providers are primarily known: Klarna, bob Finance, MF Group, SwissBilling, Byjuno and Ideal Payment. The offerings of bob Finance, SwissBilling, and Ideal Payment are available with Payrexx. In 2023, some new providers such as BNPL from TWINT (in partnership with SwissBilling) and others will drive the topic.

Trend 4: Biometric authentication becomes the standard

The use of biometric authentication methods such as facial recognition, voice analysis, and fingerprint scanning will continue to increase, and in 2023 many companies will rely on these technologies to verify user accounts and make payment transactions more secure. By using biometric data, fraud and identity theft can be prevented. Example: online retailer Amazon already allows its customers to make purchases directly using facial recognition.

Also in the field of 3-D Secure in version 2, a new approach uses biometric authentication with a broader spectrum of data. 3-D Secure is a security protocol for online payments developed by major credit card companies. It aims to increase the security of online purchases by introducing an additional security layer that is interposed on every online purchase.

Trend 5: Increase in instant payment solutions

The use of instant payment solutions will continue to increase, and the technology will become a preferred payment method for many customers and companies. Instant payment solutions allow payments to be made in real time and offer a fast and convenient alternative to traditional payment methods such as bank transfers.

By using instant payment solutions, payments can be completed within seconds, making it ideal for quick transactions, such as when purchasing products in the e-commerce sector. Another advantage of instant payment solutions is their high security. By using encrypted data transmissions and modern authentication methods such as biometric technologies, payments using instant payment solutions are very secure.

In the field of instant payments, Switzerland currently lags far behind in international comparison. Nevertheless, there are some projects and efforts to develop and promote instant payment standards. More and more banks are already offering P2P real-time payments. For example, Yapeal. Payrexx will also offer a Swiss instant payment solution for the e-commerce sector in cooperation with banks.

Trend 6: Growth of fintech companies

The number of fintech companies offering innovative payment solutions will continue to grow, and in 2023 these companies will play an important role in digital payments. Due to their focus on customer needs and their advanced technologies, they will represent an alternative to traditional banks.

There will therefore be stronger collaboration between online payment providers and traditional financial service providers.

“The payment sector is on a growth path, also because small and medium-sized enterprises, public institutions, and retailers want to integrate payment and financing options into their processes”

says PwC fundraising expert Sherin Maruhn in an interview with Reuters news agency at the end of December 2022. Source: Cash article from December 18, 2022

Trend 7: Spread of wearable payment technologies

The spread of wearable payment technologies, such as smartwatches and fitness trackers that can be used as a means of payment, is steadily increasing. These technologies allow users to make payments easily and conveniently via their wearable device by holding their device to a payment terminal or authorizing their payment via a corresponding app. An example of such a wearable payment technology is the Apple Watch. The Apple Watch can be connected to the iPhone and allows users to make payments via the Apple Pay app. Users can add their credit or debit card and then make payments in stores, restaurants, or online by holding their Apple Watch to the terminal or authorizing via the app.

Another example is Garmin Pay (headquartered in Schaffhausen) - a payment function available on most Garmin fitness trackers. Users can add their credit or debit card and then make payments in stores or online by holding their Garmin watch to the terminal or authorizing their payment via the Garmin app. The spread of wearable payment technologies offers users a convenient and secure way to make payments. These technologies also allow users to leave their physical wallets at home and still make payments, which can be particularly advantageous for athletes and people on the go.

Trend 8: Increased focus on security

In the digital payment sector, a focus on security is becoming more important as more and more people shop and make payments online. With the increasing use of technologies such as mobile payments and online banking, the risk of cyber-attacks and data misuse also increases.

To ensure the security of transactions and personal information, it is important to use secure payment methods and secure online payment providers and to perform regular security updates. The introduction of regulations and compliance standards also helps to improve security in the digital payment sector.

The PCI-DSS (Payment Card Industry Data Security Standard) Level-1 is an internationally recognized security standard developed by the Payment Card Industry Security Standards Council (PCI SSC). It sets out how companies should handle credit and debit cards securely to minimize the risk of data breaches and misuse. The PCI-DSS Level-1 standard is considered the highest security level and sets strict requirements for the management of security measures and the protection of sensitive customer data. Companies that meet the PCI-DSS Level-1 standard can ensure they offer their customers a secure payment process and protection of their personal data. The payment provider Payrexx annually meets the latest PCI-DSS Level-1 standards at the highest security level.

Trend 9: Virtual credit cards

A virtual credit card is a type of electronic payment method that allows you to make online purchases without having a physical credit card. It is created through an online account (usually via a smartphone app) with a credit card company or bank and can then be used for online payments. In addition to traditional credit cards, there are also prepaid credit cards and debit cards (Debit Mastercard, Visa Debit) as virtual cards.

Virtual credit cards usually have a limited validity period and a fixed amount that can be used for payments. They are safer than conventional credit cards because they cannot be stolen or lost, and no personal information needs to be provided to use them.

The use of virtual credit cards will increase as they offer a simple and secure way to pay for online purchases. Important advantages of virtual credit cards include:

Flexibility: Virtual credit cards can be easily created and deactivated, making them easy to manage and control.

Easy setup: There is no paperwork or waiting times to obtain a virtual credit card, as it can be set up online.

International usability: Virtual credit cards are accepted worldwide and can be easily used for online purchases and payments abroad.

Anonymity: Virtual credit cards allow payments to be made anonymously as no personal information needs to be provided.

Learn more about accepting virtual credit cards with Payrexx now. A good provider overview for consumers is available at Moneyland .

Trend 10: Growing popularity of P2P payment services and platforms

Platforms that allow users to make direct payments to each other will continue to gain popularity for the following reasons:

Convenience: P2P payment platforms allow users to send and receive payments directly from their smartphones or computers without the need for cash or checks.

Security: P2P payment platforms often use security assumptions such as encryption and secure authentication to protect users’ financial information.

Wide acceptance: Many P2P payment platforms are widely accepted and used by many people, making it easy to send and receive payments from others.

Cost: P2P payment platforms can be more cost-effective compared to traditional payment methods as they often have lower or no fees.

Social payments allow users to donate money and send and receive money to and from friends and family, directly via social networks like Facebook and Instagram or payment services like TWINT, Paypal, or increasingly via Neon bank apps.

This type of payment is likely to become even more important in the future, especially among younger users.

Trend 11: Omnichannel payments

More and more customers are shopping via different channels and devices. Omnichannel payments enable companies to provide their payment options for all channels, thus improving user-friendliness and customer satisfaction. They also make it easier for customers to make payments, whether they shop online or in a store, and allow payments to be tracked and managed across different devices. Omnichannel payments thus help to improve the customer experience and strengthen customer loyalty.

Trend 12: Increasing use of blockchain technology for micropayments

In recent years, the use of cryptocurrencies such as Bitcoin, Ethereum, and Litecoin as a means of payment, especially for micropayments, has become increasingly widespread, and this trend will continue in 2023.

Given the current events, it is easy to forget that the crypto industry has also developed strongly in recent months regardless of market turmoil. With The Merge, the Ethereum ecosystem has seen a significant technological advance that will improve the scalability and mass suitability of the Ethereum blockchain.

Blockchain technology has the potential to be used as a new standard for micropayments, as it enables fast, secure, and cost-effective transactions. With Centi Payment Services (Centi Ltd), there is an interesting project in Switzerland that allows micropayments in real time and almost without costs.

Central bank digital currencies (CBDC) on the rise

CBDCs (Central Bank Digital Currencies) are digital currencies issued by central banks. They are often considered a potential alternative to traditional currencies and could play an important role in digital payments in the future.

There are several reasons why CBDCs are considered future opportunities in the digital payments sector. First of all, they are faster and more cost-effective than traditional payment methods, as they can be transferred directly between two parties without the need for intermediaries. They can also serve as a means to promote financial inclusion by providing people without a bank account or with poor credit access to financial services.

However, there are also some challenges to consider when introducing CBDCs. For example, there are privacy concerns as central banks may have access to financial transactions made with CBDCs. There are also questions in the context of regulation and dealing with cyber risks.

Globally, there are two major mega-trends (mega-trend transparency and mega-trend globalization) driving the digital transformation. No one can oppose these trends — they are the “flow of history” of our society. In view of this, as well as the fact that new CBDC projects are published daily, the Swiss National Bank (SNB) as an innovative national bank in Central Europe must join in.

Although SNB Governing Board member Andrea Maechler said at an online financial conference at the Goethe University in Frankfurt on January 18, 2022, that the SNB rejects a central bank digital currency (CBDC) for private individuals for broad use for everyday transactions because it believes that the risks outweigh the benefits, we at Payrexx are convinced that a digital Franc will be introduced in the foreseeable future.

Further information on this topic:

Conclusion

Overall, 2023 will be an exciting year for the digital payments industry, with numerous new developments and innovations. We can be eager to see what new products and technologies the industry will expect in the coming months.

Disclaimer: The opinions expressed in this article on trends in the digital payment market reflect the personal opinions of the experts at Payrexx AG and may not be complete or correct.

Create your own successes with Payrexx

Payrexx offers a simple and convenient payment solution, allowing your customers to easily choose their preferred payment method, as well as an optimized checkout to increase your conversion rate.

As one of the fastest-growing payment service providers in the German-speaking region, we have made it our task to empower our customers with the tools they need to be more successful in e-commerce. At Payrexx, you can expect advanced security features, all popular payment methods such as TWINT, Mastercard, VISA, PostFinance, Apple Pay, Google Pay, Samsung Pay, Paypal, and QR billing from a single source. Also an intuitive Dashboard with integrated e-commerce tools, as well as personal support for all business phases.

Learn more about secure online payments with Payrexx now.