“Buy now, pay later” – Opportunities and risks for online shops

Anyone shopping online wants to be able to pay flexibly. This not only includes a wide selection of payment methods, but also the timing of the transaction needs to be chosen. Increasingly, customers are demanding the so-called 'Buy now, pay later' model: buy now, pay later. We answer the most important questions.

Sheila

Matti

Actually, this payment model has been around for a while: Before the heyday of online trading, we used to select our goods from a catalogue, order the desired items to our home and only pay for them once they arrived by post. Buy now, pay later was the motto then as it is today. However, the term “Buy now, pay later”, abbreviated BNPL, encompasses much more than just purchase by invoice.

When a customer chooses the BNPL payment option, a complex and fully automated process is initiated in the background. For someone to pay for their goods later, their creditworthiness must first be checked. Within seconds, it is determined whether the buyer is authorised to pay or not. Another difference from the conventional purchase by invoice is that instalment payments are often offered with BNPL: A new LED widescreen television for just 100 EUR per month? Convenient!

What are the benefits of Buy now, pay later?

Customers benefit in various ways from “Buy now, pay later”: For instance, they can order several versions of a type of shoe, try them on and ultimately only pay for the pair that fits. They simply send the rest back. Alternatively, they might treat themselves to a high-priced product that wouldn't be feasible to finance outright, but is possible in instalments. Buy now and pay later therefore means not just more flexibility, but also more freedom for the buyer.

For online merchants, the advantages of BNPL lie particularly in customer retention. The aspect of trying out reduces the customer's hesitation, leading them more often to complete the purchase process and feel more comfortable at checkout. When an online shop shows trust to its customers, it is demonstrably reciprocated. Various market studies have shown that the BNPL option not only increases the volume of the shopping basket but also the number of purchases.

How is Buy now, pay later developing?

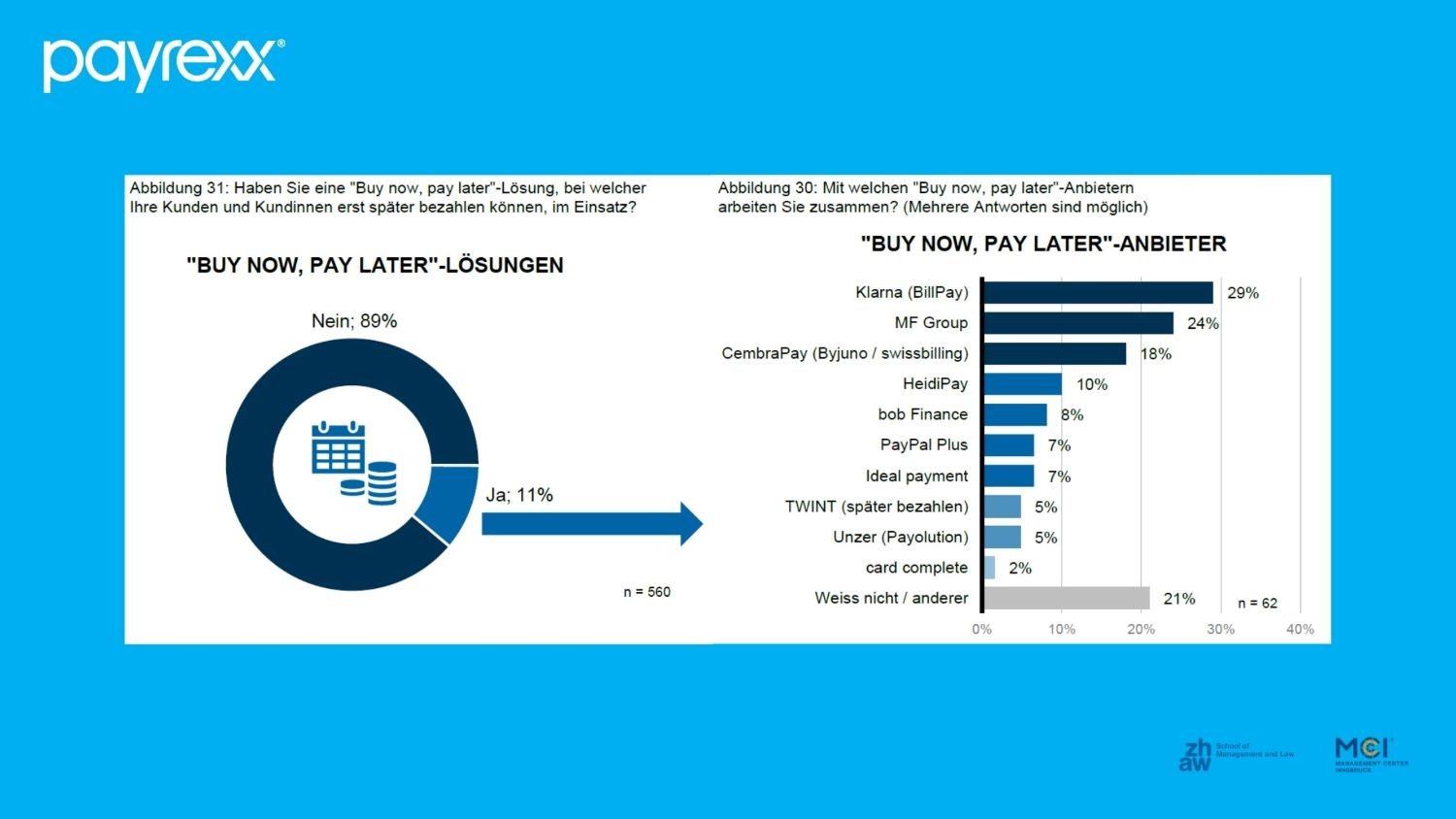

In Asia and America, “Buy now, pay later” is experiencing impressive growth and demand is also steadily increasing in Europe. However, in Switzerland, there's still plenty of room for improvement: In the 2023 Online Merchant Survey by the Institute of Marketing at ZHAW, only 11 percent of the 598 participating online merchants stated they offer BNPL to their customers. This represents a decrease compared to the previous year, when 17 percent had such a solution integrated in their shop.

According to the survey, it is primarily online shops with an average large shopping basket that offer BNPL. The volume being talked about is 500 francs or more. Thus, instalment and invoice purchases seem particularly sensible when an online shop mainly offers high-priced goods, such as furniture, electronic or kitchen appliances, travel, or branded clothing.

It's also noticeable that when a shop offers BNPL, the payment model becomes increasingly important for its customers. 10 percent of online merchants with a BNPL model reported that instalment payments are increasing significantly. At 25 percent, at least slight growth was recorded. In 29 percent of shops with BNPL, the share of instalment payments remained about the same, and only 6 percent saw the payment model lose significance. This shows that “Buy now, pay later” is also becoming increasingly popular in Switzerland.

Who bears the arising risk?

“Buy now, pay later” offers an online shop and its customers not only various benefits but is indeed associated with certain risks. What happens, for example, if the goods are shipped but never paid for? And with what money is the gap filled that arises from the delayed payment?

If a customer opts for the BNPL payment option, they legally receive the ownership rights to the acquired product immediately – regardless of whether they pay the money directly, later, or in instalments. This is only possible thanks to an external provider who effectively pre-finances the transaction and transfers the amount to the online shop on behalf of the customer. To some extent, the BNPL service provider grants end consumers a credit. It is ultimately this company that collects the money from the buyer and is thus responsible for ensuring that the amount is actually transferred.

Reminders, warnings, threats of legal action – all these measures are taken over by the external provider in an emergency. In return, they usually charge a fixed fee on every purchase made through “Buy now, pay later”. For the online shop itself, this results in no financial risk.

Which BNPL providers exist in Switzerland?

In addition to several large international providers such as Klarna or the MF Group, there are also various companies from Switzerland that specialise in “Buy now, pay later”. Two of them are integrated into the Payrexx solution, allowing you as a Merchant to quickly and easily hop on the BNPL train.

Active in the Swiss market since 2020 is HeidiPay, a simple card-based payment solution focusing on instalment payments, allowing goods to be paid over 24 months. While the customers can pay over time, the Merchant is immediately paid by HeidiPay. Depending on the online shop, HeidiPay offers a different package, but Payrexx handles the initial contact for you: Simply select as a payment provider, and HeidiPay will get in touch with you!

The 2023 Online Merchant Survey of the Institute of Marketing from ZHAW shows that few online merchants use BNPL. The most popular provider is Klarna.

Also recently, the increasingly popular payment system TWINT in Switzerland offers a “Buy now, pay later” solution. With “TWINT pay later” you offer your customers the option to pay for their purchases up to 30 days later. Here too, TWINT handles the initial payment and any potential risk. As a Payrexx customer, you can apply for this BNPL system through a form – we then handle the setup with TWINT for you, so activation is quick and easy.

Thanks to Payrexx, entering the rapidly growing world of BNPL payments becomes child's play. To ensure your customers' trust is not diminished, you can also process all payment steps under your own brand identity. Your users feel secure in the familiar environment, and you as a Merchant benefit from a reliable Payment Service Provider (PSP) that allows you to offer another payment method – without any risk, but with maximum flexibility.